Little Known Questions About Mortgage Investment Corporation.

Table of ContentsThe Single Strategy To Use For Mortgage Investment CorporationTop Guidelines Of Mortgage Investment CorporationThe Definitive Guide to Mortgage Investment CorporationThe Ultimate Guide To Mortgage Investment Corporation

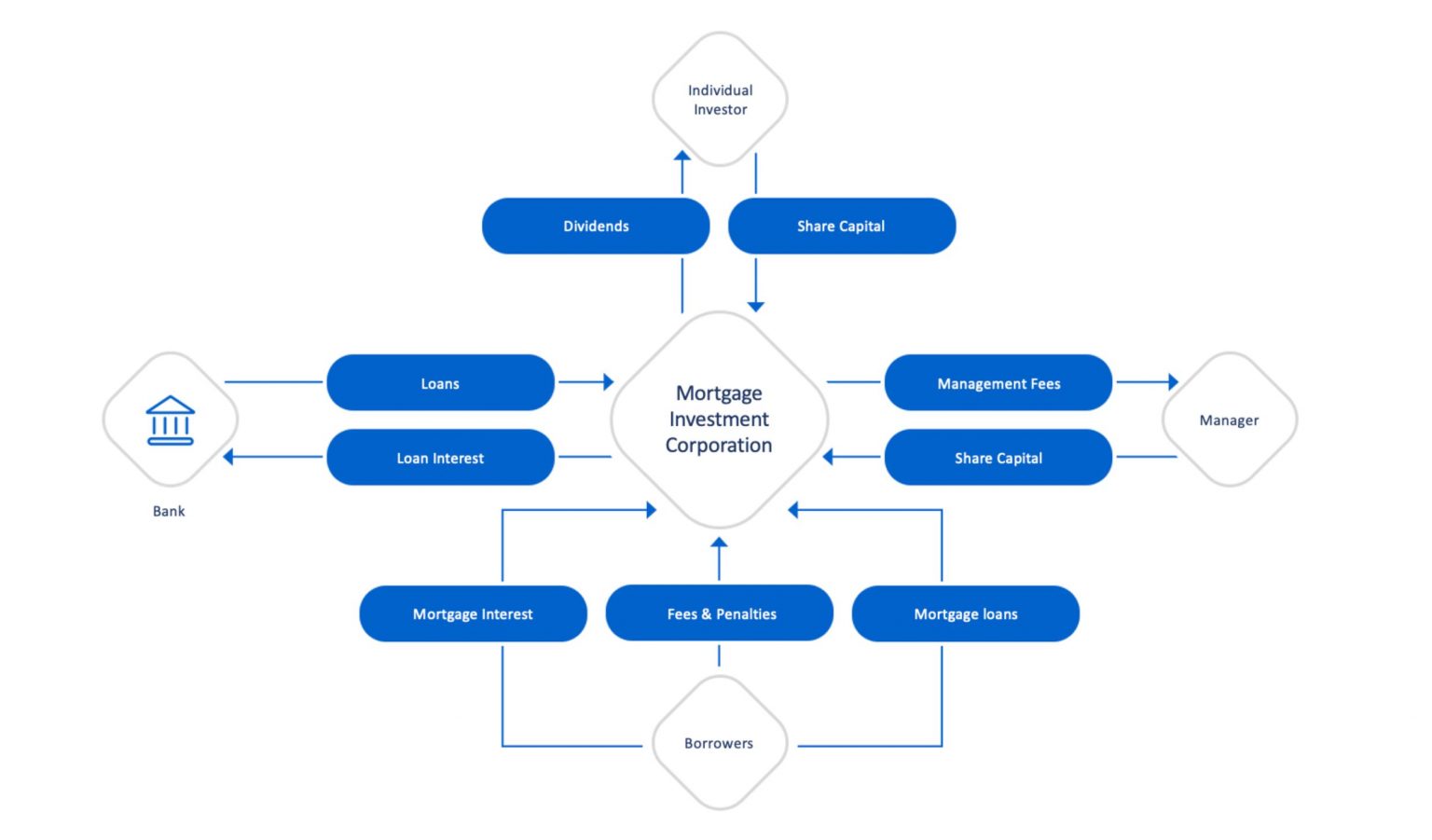

Exactly How MICs Resource and Adjudicate Loans and What Takes place When There Is a Default Home loan Financial investment Firms provide financiers with straight exposure to the realty market through a pool of meticulously picked home mortgages. A MIC is in charge of all aspects of the mortgage investing process, from origination to adjudication, including daily management.

We invest in home loan markets throughout the nation, allowing us to provide throughout Canada. To get more information concerning our financial investment process, get in touch with us today. Call us by filling in the type listed below to learn more regarding our MIC funds.

A MIC is additionally considered a flow-through financial investment lorry, which means it has to pass 100% of its yearly earnings to the investors. The rewards are paid to investors regularly, typically each month or quarter. The Revenue Tax Obligation Act (Area 130.1) information the needs that a firm must meet to qualify as a MIC: At the very least 20 shareholdersA minimum of 50% of properties are residential mortgages and/or cash deposits insured by the Canada Down Payment Insurance Policy Firm (CDIC)Much Less than 25% of resources for each and every shareholderMaximum 25% of resources spent right into actual estateCannot be associated with constructionDistributions filed under T5 tax formsOnly Canadian mortgages are eligible100% of take-home pay mosts likely to shareholdersAnnual monetary statements investigated by an independent bookkeeping firm The Mortgage Financial investment Firm (MIC) is a specialized financial entity that invests largely in mortgage.

The Best Guide To Mortgage Investment Corporation

At Amur Resources, we aim to give an absolutely diversified technique to alternate financial investments that optimize yield and funding preservation - Mortgage Investment Corporation. By using a range of traditional, income, and high-yield funds, we satisfy a range of investing purposes and preferences that match the requirements of every private capitalist. By buying and holding shares in the MIC, investors obtain a proportional possession interest in the company and receive revenue with dividend payments

On top of that, 100% of the investor's capital gets positioned in the selected MIC without any ahead of time transaction fees or trailer fees. Amur Funding is concentrated on offering capitalists at any degree with access to properly managed personal mutual fund. Financial investment in our fund offerings is available to Alberta, British Columbia, Manitoba, Nova Scotia, and Saskatchewan citizens and must be made on a personal placement basis.

Spending in MICs is a great method find to get direct exposure to Canada's flourishing realty market without the needs of energetic residential or commercial property administration. Apart from this, there are numerous various other reasons investors consider MICs in Canada: For those seeking returns comparable to the securities market without the connected volatility, MICs supply a protected realty financial investment that's less complex and might be extra profitable.

Actually, our MIC funds have traditionally delivered 6%-14% annual returns. * MIC financiers obtain dividends from the rate of interest payments made by borrowers to the home loan lending institution, forming a constant easy income stream why not try here at higher rates than standard fixed-income securities like government bonds and GICs. They can likewise select to reinvest the rewards right into the fund for worsened returns.

Little Known Facts About Mortgage Investment Corporation.

MICs currently account for roughly 1% of the overall Canadian mortgage market and stand for an expanding sector of non-bank economic business. As financier need for MICs expands, it is necessary to understand how they function and what makes them various from typical property investments. MICs purchase home mortgages, not genuine estate, and as a result supply exposure to the housing market without the included danger of building possession or title transfer.

usually between six and 24 months). In return, the MIC gathers rate of interest and charges from the debtors, which are after that distributed to the fund's chosen shareholders as returns repayments, commonly on a month-to-month basis. Due to the fact that MICs are not bound by a lot of the exact same strict financing needs as typical financial institutions, they can set their own standards for accepting loans.

This means they can bill greater rate of interest rates on home mortgages than standard banks. Mortgage Investment Corporations additionally appreciate special tax therapy under the Income Tax Obligation Work As a "flow-through" financial investment car. To avoid paying revenue taxes, a MIC must disperse 100% my review here of its take-home pay to shareholders. The fund has to contend least 20 investors, with no investors having greater than 25% of the impressive shares.

The Definitive Guide to Mortgage Investment Corporation

Instance in point: The S&P 500's REIT classification greatly underperformed the more comprehensive stock exchange over the past five years. The iShares united state Property exchange-traded fund is up less than 7% because 2018. Comparative, CMI MIC Funds have traditionally created anywhere from 6% to 11% annual returns, depending upon the fund.

MICs give investors with a way to spend in the actual estate sector without actually owning physical residential property. Rather, capitalists merge their money with each other, and the MIC utilizes that cash to money home mortgages for consumers.

That is why we intend to aid you make an informed decision regarding whether or not. There are many advantages related to buying MICs, consisting of: Given that investors' cash is merged with each other and spent throughout several homes, their portfolios are branched out across different property kinds and consumers. By possessing a profile of mortgages, investors can reduce danger and avoid putting all their eggs in one basket.